- Collegamento all'originale")

9th Global Conference on Illegal Finance and Crypto

The following is a report from PPI´s representative at the United Nations Office of Vienna, Mr. Kay Schroeder, who attended the UNODC Conference on Illegal Finance and Crypto.

Reflections from the 9th Global Conference on Criminal Finance and Crypto – UN Vienna

Yesterday I attended the 9th Global Conference on Criminal Finance and Crypto, hosted at the

United Nations in Vienna with support from UNODC. While no official UN representatives were

present, the event offered a revealing glimpse into how private sector challenges—particularly those

surrounding crypto finance—are increasingly reframed as matters of public concern.

The conference celebrated the growing institutional acceptance of crypto assets, shifting the

narrative from speculative private losses to regulated public affairs. This reframing was not just

semantic—it was strategic. Legal frameworks now position crypto as a legitimate asset class,

despite its origin as replicable code. The symbolic elevation of crypto into the realm of public

policy raises fundamental questions about value, legitimacy, and institutional responsibility.

At its core, blockchain technology is designed to reduce transaction costs. Its native tokens—like

BNB on the Binance Smart Chain—are meant to facilitate efficiency, not store value. Yet the market

treats these tokens as assets, creating artificial scarcity and speculative value.

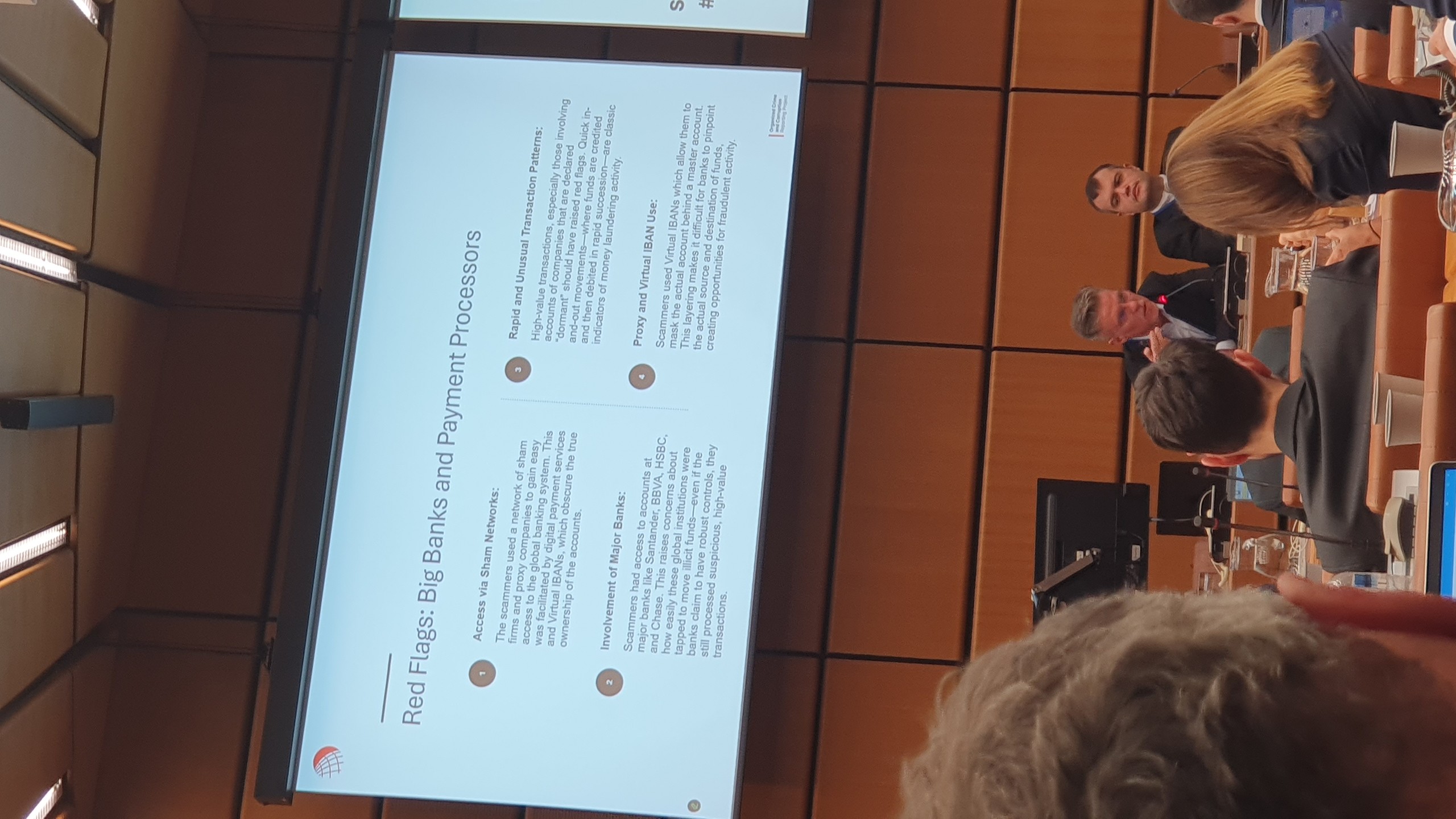

This contradiction was starkly illustrated during a presentation by Francesco Venditti, who proudly described the

seizure of BNB as a value store, while simultaneously labeling a lesser-known BEP-20 token as a

rug pull. Ironically, the logic of blockchain suggests the opposite: BNB should devalue with

increased use, while any token’s value depends on its legal and economic framing.

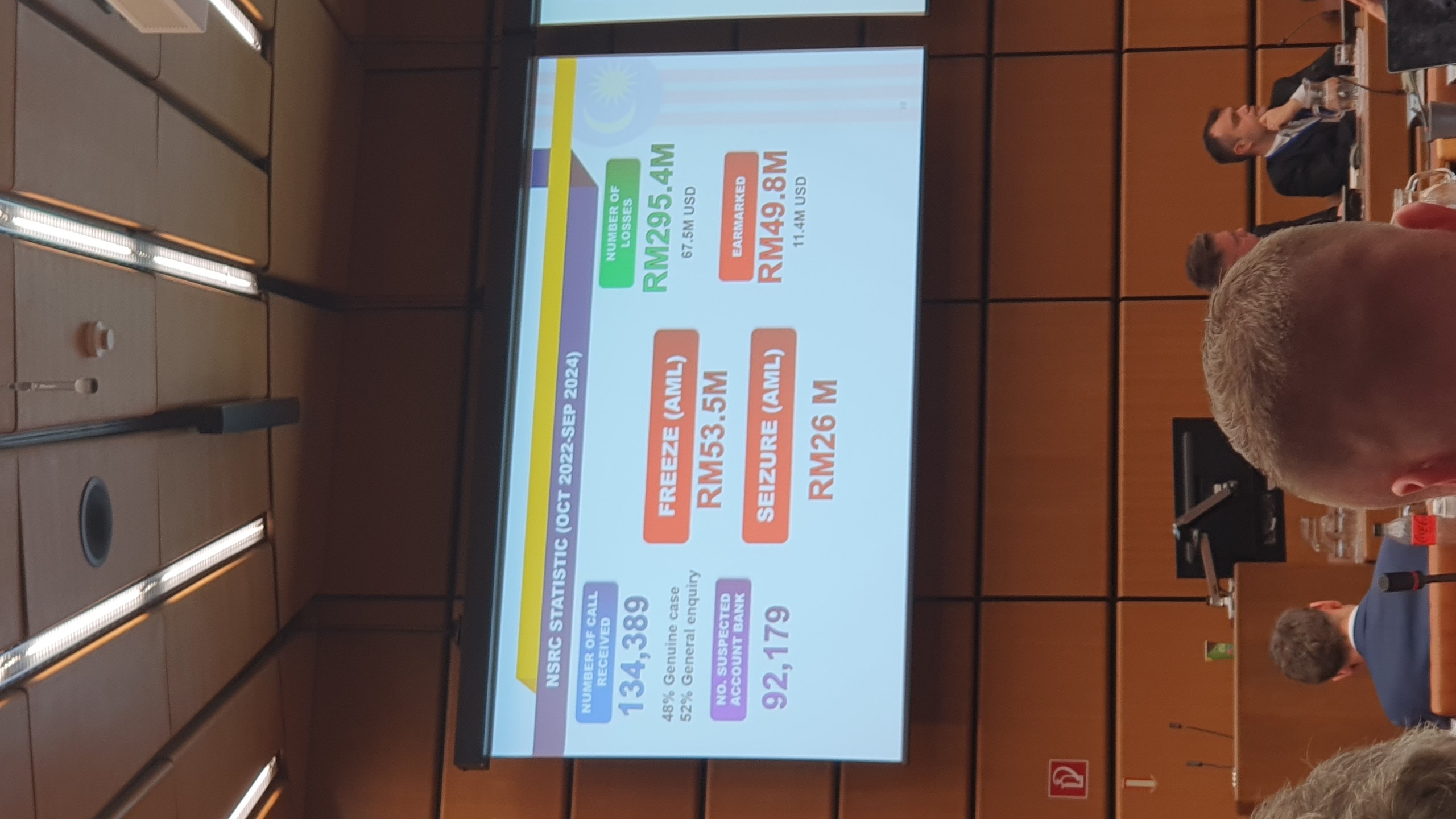

The deeper issue lies in the off-chain dominance of crypto transactions—estimated at 80–90%—

which undermines the transparency and decentralization that blockchain promises. Centralized

exchanges (CEXs) and DeFi platforms act as both gatekeepers and service providers, facilitating

flows that often bypass the very technology they claim to represent. This dual role complicates

efforts to combat illicit finance, especially when the same actors who enable laundering also claim

to fight it.

Stablecoins deserve particular scrutiny. Pegged 1:1 to fiat currencies, they are technically simple

tokens maintained off-chain. They are not cryptocurrencies in the traditional sense, but rather

symbolic representations of fiat value. Their presence in blockchain ecosystems injects artificial

stability into systems designed to devalue through scalability. In this sense, stablecoins function as

Trojan horses—vehicles through which the fiat system reasserts control over decentralized

infrastructure.

The economic implications are profound. Blockchain tokens represent a new category of economic

goods—ones that devalue with increased use. This defies conventional market logic, where utility

and demand typically reinforce value. If transaction costs approach zero, and those costs are tied to

the token itself, then the token’s value must also approach zero. Yet institutional actors continue to

frame these tokens as stores of value, creating a performative economy that contradicts its own

technological foundations.

During the conference, I posed a question to the panel of lawmakers and lobbyists exploring

solutions to “illegal finance and crypto”:

“What is your opinion on forbidding stablecoins to remove the artificial valuation of

blockchain tokens, which naturally devalue due to scaling requirements?”

The question remains open. But the conversation is shifting—from retail scams to structural

manipulation, from private speculation to public framing. As crypto continues its institutional

ascent, we must remain vigilant about the symbolic and economic contradictions embedded in its

architecture.”

pp-international.net/2025/10/i…